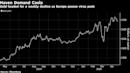

(Bloomberg) -- Gold headed for its largest weekly decline in seven weeks as European nations, including the U.K., offered cautious signals they’ve passed through the peak of the coronavirus outbreak and as U.S. cases rose at the slowest pace this month.U.K. Prime Minister Boris Johnson said the country was through the worst of the virus and pledged to deliver plans to lift the lockdown, while Italy, France and Germany all also outlined proposals to gradually ease restrictions. The European Central Bank stepped up its response to the coronavirus crisis by cutting funding costs for banks, but refrained from boosting its bond-buying program.“Demand for safe haven assets took a further dive” after Johnson’s virus comments Thursday in the U.K., Australia & New Zealand Banking Group Ltd. economist Kishti Sen said Friday in a note. Asian trading was limited Friday, with much of the region out on holidays.Spot gold was steady at $1,687.29...

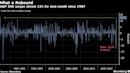

(Bloomberg) -- U.S. futures slid along with Japanese and Australian shares, and the dollar climbed, after sobering comments from Amazon and Apple about the impact of the coronavirus.Amazon.com warned of a possible second-quarter loss, while Apple omitted an earnings forecast for the first time in more than a decade. While global stocks posted their best month since 2011 in April -- spurred by a slowdown in coronavirus infections and massive stimulus initiatives -- earnings announcements and economic data are serving a reminder of lasting pain. The dollar halted a four-day slide and Treasuries recouped some recent losses amid the risk-off tone Friday. Trading was limited by holidays across much of the Asian region, and most of Europe will also be shut.Strong results from Microsoft Corp., Facebook Inc. and Tesla Inc. had limited losses on the tech-heavy Nasdaq gauges on Thursday. The S&P 500 Index posted its best month since 1987.Investors continue...

Oil slipped to around $26 a barrel on Friday as weak demand due to the coronavirus crisis and excess supply pressured the market, even as OPEC and its allies began a record output cut. The global oil benchmark, Brent crude, has collapsed 60 percent in 2020 and reached a 21-year low last month as the coronavirus pandemic squeezed demand and OPEC and other producers pumped at will before reaching a new supply cut deal which began on Friday. Brent for July fell 46 cents, or 1.7%, to $26.02 at 0825 GMT....

Oil prices rose on Friday, extending the previous session's gains, as major producers began output cuts to offset a slump in fuel demand triggered by the coronavirus pandemic while data showed U.S. crude inventories grew less than expected. U.S. crude for June delivery rose 34 cents, or 1.8%, to $19.18 a barrel, having gained 25% in the previous session. Reflecting the output cuts agreed between OPEC and other major producers like Russia, a grouping known as OPEC+, the imbalance between oil supply and demand is to set to be halved to 13.6 million barrels per day (bpd) in May, and drop further to 6.1 million bpd in June, according to Rystad Energy....

Oil prices rose on Friday, extending the previous session's gains, as major producers began output cuts to offset a slump in fuel demand triggered by the coronavirus pandemic while data showed U.S. crude inventories grew less than expected. Also supporting prices was data from the U.S. Energy Information Administration data showing crude inventories rose by 9 million barrels last week to 527.6 million barrels, less than the 10.6 million-barrel rise analysts had forecast in a Reuters poll....

Oil prices jumped on Friday, extending the previous session's gains, buoyed by a lower-than-expected gain in U.S. crude inventories and the start of output cuts in a bid to offset a slump in fuel demand triggered by the coronavirus pandemic. Brent crude for July delivery, which started trading on Friday as the new front-month contract, was up $1.10, or 4.2%, at $27.58 a barrel by 0013 GMT. Brent gained 12% on Thursday....

(Bloomberg) -- The Federal Reserve revamped its Main Street Lending Program in ways that will allow battered oil companies to qualify for the aid after industry allies lobbied the Trump administration for changes.Larger, more heavily indebted companies can now qualify and use the money to pay off prior loans under the changes the central bank announced Thursday.The move opens the door to more oil and gas producers, said Senator Kevin Cramer, a Republican from North Dakota, who had pressed the administration on the issue as energy companies struggle to survive an epic collapse in fuel demand and crude prices.“With the decrease in demand and oversupply due to the global oil price war creating a valley for these highly leveraged companies, this expansion will help them bridge the gap as we look to reopen America,” Cramer said in an emailed statement Thursday.Environmentalists blasted the shifts they said rewarded oil companies that took...